If you’re looking for a new home but are having trouble getting a loan preapproval, owner financing is an option that can help you achieve your goal of homeownership. Though not all sellers will be willing to offer direct financing to the purchaser, it can be a great way to buy a home while also making the closing process go more smoothly. Owner-financed homes, on the other hand, can be complicated and require a written agreement, so it’s critical to understand the system before signing on the dotted line. We’ll go over how owner financing works, how it can benefit you as a buyer or seller, and how to structure a deal with an owner.

9+ Owner Finance Contract Samples

A transaction in which the seller of property funds the purchase directly with the person or group that is buying it, in whole or in part, is known as owner financing. Because it eradicates the costs of a bank intermediary, this type of arrangement can benefit both sellers and buyers. Owner financing, on the other hand, can expose the owner to far more risk and responsibility.

1. Owner Finance Contract Template

2. Owner Finance Form Contracts

3. Owner Financed Farm Sales Contract

4. Pace Lender Owner Finance Contract

5. Owner Financing Seller Contract

6. Form Pace Owner Finance Contract

7. Owner Finance Consumer Protection Contract

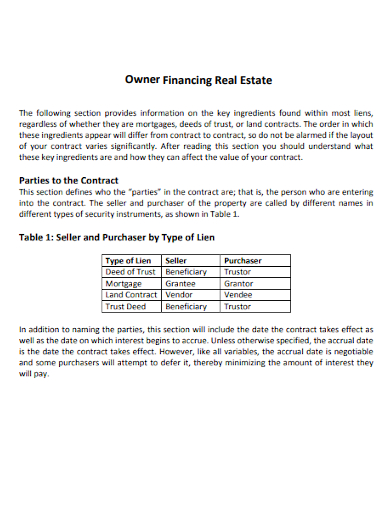

8. Owner Financing Real Estate Contract

9. Owner Finance Purchase Contract

10. Owner Financing Contract for Sale

How Owner Financing Works

Owner financing, like a traditional mortgage, entails putting a down payment on a home and paying off the rest over time. This alternative to traditional financing, on the other hand, is generally more expensive and needs repayment or refinancing into a traditional loan in as little as five years. Even so, if the seller is willing and able to provide it, seller financing is usually faster and more efficient to obtain than a government-backed mortgage.

While most owner financing entails some form of background or credit check, it can assist otherwise unqualified borrowers in becoming homeowners. Not only are no banks or traditional lenders involved, but owner financing does not require a checking or appraisal unless the buyer requests it.

After a buyer and seller agree on terms, the owner-seller receives monthly payments according to a consented amortization schedule. The borrower may also be faced with a large lump-sum fee at the end of the loan term, depending on the schedule. Unlike traditional mortgages, however, tax and insurance payments are typically not rolled into monthly debt service and must be paid separately by the buyer.

The purchaser either makes the balloon payment or acquires a mortgage refinance and pays off the suppliers with the money collected from a new loan at the end of the loan term. The buyer will either receive title to the property for the first time or the seller will implement a Satisfaction of Mortgage stating the mortgage has been paid in full and releasing the lien on the property, depending on how the owner financing was originally structured.

FAQs

What are the requirements of owner financing?

A promissory note should be used to facilitate an owner-financing transaction. The promissory note outlines the terms of the agreement, including the interest rate, repayment schedule, and default penalties, among other things. To protect himself against default, the owner usually keeps the property title until all payments have been made.

While some do-it-yourself transactions can be handled entirely by the owner, hiring an attorney to ensure that all of the bases are covered is usually a good idea. Paying for a title search can also help to ensure that the owner/seller is in a position to sell the property and that they will eventually release the title in exchange for financing some or all of the transaction.

What are the pros and cons of owner financing to sellers?

Pros:

- Can sell “as is”: There’s a chance you’ll be able to sell without having to make costly repairs that traditional lenders might demand.

- A good investment: You may be able to earn higher rates on the money you raise from the sale of your home than you would if you invested it elsewhere.

- Option to sell the promissory note for a lump-sum payment: The promissory note can be sold to an investor for a lump-sum payment right away.

- Keep title if the buyer defaults: If the buyer defaults, you keep the down payment, any money paid, and the house.

- Sell faster: Because buyers avoid the mortgage process, you may be able to sell and close faster.

Cons:

- Dodd-Frank Wall Street Reform and Consumer Protection Act: The Dodd-Frank Wall Street Reform and Consumer Protection Act imposed new rules on owner financing. Depending on the number of properties the seller owner-finances each year, balloon transactions may not be an option, and you may need to work with a mortgage loan originator.

- Default: The buyer has the option to stop paying at any time. If this occurs and they do not simply walk away, you may be forced to go through the foreclosure process.

- Repair costs: Depending upon how the buyer took care of the property, you may have to pay for repairs and maintenance if you take back the property for whatever reason.

What are the pros and cons of owner financing to buyers?

Pros:

- Can give a borrower access to money they wouldn’t have been able to get otherwise.

- Allows buyers to finance homes that would otherwise be ineligible for conventional financing.

- Allows buyers and sellers to speed up the due diligence process for a faster closing.

- Reduces closing costs by obviating the need for appraisals, bank fees, and—if the buyer so desires—inspection fees.

- Minimum down payment requirements for government-backed mortgages are repealed.

Cons:

- When compared to a traditional mortgage, it frequently has higher interest rates.

- Borrowers may be required to pay a balloon payment at the end of the loan term.

- The seller may or may not be willing to provide owner financing depending on the borrower’s creditworthiness.

- A due-on-sale clause in the seller’s mortgage may require them to pay off the mortgage when they sell the house, preventing them from offering owner financing.

If you’re thinking about owner financing, you should consult with a real estate lawyer who can represent you during agreements and evaluate the contract to ensure that your rights are protected.

Related Posts

Sample Excuse Letter for School

Feature Writing Samples

FREE 10+ Security Guard Contract Samples in PDF | MS Word

FREE 10+ Option to Purchase Agreement Samples in MS Word | Apple Pages | PDF

FREE 26+ Curriculum Form Samples in MS Word | PDF

FREE 20+ Cleaning Service Proposal Samples in PDF | MS Word

FREE 29+ Sample Loan Application Form Templates in MS Word | PDF

FREE 10+ Event Venue Contract Samples in PDF | MS Word | Pages | Google Docs

FREE 10+ SBAR Samples in PDF | DOC

FREE 12+ Music Band Contract Templates in PDF | MS Word

FREE 10+ HVAC Maintenance Contract Samples in PDF | MS Word

FREE 10+ Social Media Marketing Contract Samples in MS Word | PDF

FREE 10+ Wholesale Assignment Contract Samples in PDF

FREE 18+ Financial Proposal Samples in PDF | MS Word | Google Docs | Pages

FREE 10+ Feasibility Study Samples in PDF