Lacking the appropriate financial means, can delay your project. Don’t be too quick on the draw, there is a process for everything including financing your commercial construction projection. Project financing involves soliciting a proposal from a financial institution, carefully reviewing the terms and conditions of that proposal, obtaining a satisfactory appraisal, ensuring clear title to the property and then closing on the loan. Because it is becoming increasingly difficult to obtain commercial construction loans, it only makes good sense to present yourself well. One of the best ways to improve your chances of obtaining a loan is to prepare a well-written proposal.

3+ Construction Loan Proposal Samples

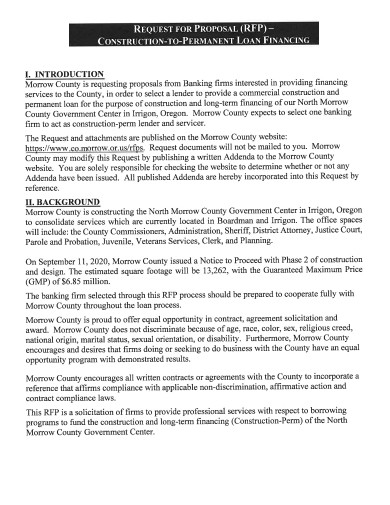

1. Construction Loan Proposal

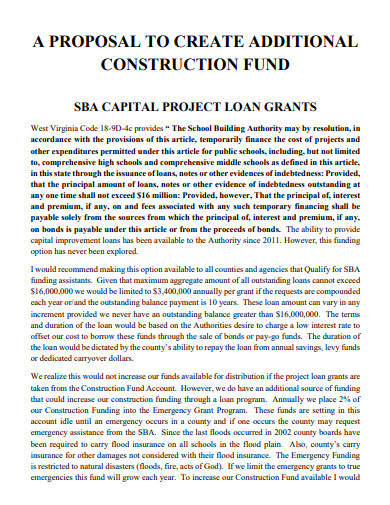

2. Sample Construction Loan Proposal

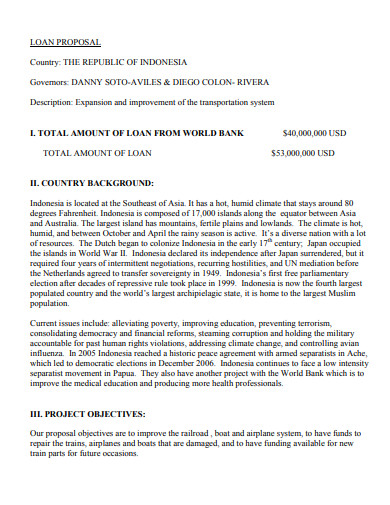

3. Simple Construction Loan Proposal

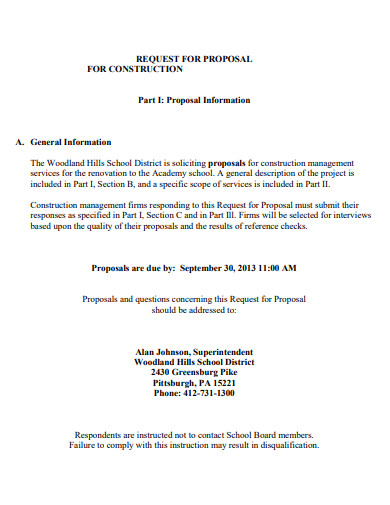

4. Construction Loan Proposal Example

What Is a Construction Loan?

A construction loan (also known as a “self-build loan”) is a short-term loan used to finance the building of a home or another real estate project. The builder or home buyer takes out a construction loan to cover the costs of the project before obtaining long-term funding. Because they are considered relatively risky, construction loans usually have higher interest rates than traditional mortgage loans.

Details to Include in a Construction Loan Proposal

1. Project description

Begin by spelling out the purpose of the commercial construction loan. Describe the type of commercial project you envision and why it is needed. State the amount of money required and why you need this amount to achieve the business purpose you have in mind. Will this building be for a single user (a company using it for its own use) or will the building be leased out to various tenants? For a single use building, the company is the sole tenant, which makes the proposal easier. For multi-tenant buildings, pre-leasing becomes a factor. Letters of intent are not good enough for multi-tenant proposals. In today’s market, lenders want to see signed pre-leasing agreements. In addition, you should provide all pertinent general information about your business. This would include the business name, name of principals, Social Security number of each principal, and your business address.

2. Equity investment

Loan applicants must have a reasonable amount of their own money invested in the project. There will be an examination of the debt-to-worth ratio of the applicant to understand how much money the lender is being asked to lend in relation to how much the owner has invested. For a single-user property, the requirement may be 30 percent down. This equity portion may be achieved by raising funds from individual investors. The lending institution wants to know about the financial strength of the equity partners. If your investors are willing to personally guarantee the loan, this needs to be stated in your proposal.

3. Business description

In this section, explain the history and nature of your business. You should provide details about what kind of business it is, the age of the business, number of employees, and current business assets. Also detail the company’s legal ownership structure. Is it a C-Corporation, an S-Corporation, a limited liability corporation (LLC), a partnership, a limited partnership, a sole proprietorship, or some combination of each?

4. Market information

Lenders want to know about where the project fits into a market. The proposal should clearly define your company’s products or services as well as your markets. Identify who the competition is and explain how your business competes in the marketplace. You will need to profile your customers and explain how your business can satisfy their needs.

5. Cash flow

Being profitable is great, but profitability does not equal cash flow. You will need to be able to demonstrate your ability to repay the loan from your business operations. For this reason you will need to provide a cash flow projection, broken out on a monthly basis. The lender will want to see that you will be able to meet all your financial obligations as they come due, not just the loan payments. Cash flow statements provide insight needed to understand more clearly how the company is protecting its operating flexibility.

6. Working capital

Firms need working capital to work well. Lenders are on the lookout for poor liquidity ratios because those are danger signals. Lending institutions often look at your current ratio (current assets divided by current liabilities) to determine your creditworthiness.

7. Financial information

For a typical commercial loan, lenders will want to see audited and review financial statements, namely your balance sheets and income statements for the past three years. In addition, the lender will want to see pro formas and budgets for the next five to 10 years. You will need to explain your assumptions for projecting revenues. What rental rates did you use? What were the vacancy factors? The lender will be examining these to make sure they are reasonable. You also will need to provide personal financial statements on yourself and other principal owners of your business. In addition to the investors, the lending institution may want to know about the financial position of the contractors you are using to build the project.

8. Management profile

And finally, never forget that people lend money to people. Lenders are attracted to management teams that have proven business experience, preferably with accountability for profit and loss. If you have a track record of increasing sales and profits, so much the better. You should include a short statement on each principal in your business. Include information on their business background, education, experience, skills, and accomplishments.

FAQs

How does a construction loan works?

Construction loans are usually taken out by builders or a homebuyer custom-building their own home. They are short-term loans, usually for a period of only one year. After construction of the house is complete, the borrower can either refinance the construction loan into a permanent mortgage or obtain a new loan to pay off the construction loan (sometimes called the “end loan”). The borrower might only be required to make interest payments on a construction loan while the project is still underway. Some construction loans may require the balance to be paid off entirely by the time the project is complete

If a construction loan is taken out by a borrower who wants to build a home, the lender might pay the funds directly to the contractor rather than to the borrower. The payments may come in installments as the project completes new stages of development. Construction loans can be taken out to finance rehabilitation and restoration projects as well as to build new homes.

Do construction loans cover the design phase of home construction?

No. Prospective custom home builders have to self-finance the design phase of the home building contract. In addition, before you can take out a construction loan, you’ll need to produce a builder’s contract, construction timetable, designs and a realistic budget. All this needs to be done even before beginning the loan application process.

Are there higher qualification requirements for construction loans?

Yes, construction loans often come with higher qualifying standards in terms of credit score requirements and down payment amounts. Usually a minimum 20% down payment is required, and a 25% down payment requirement is not uncommon. In addition, most construction loans require a minimum credit rating of 620.

Related Posts

Title Project Proposal Samples [ Community, School, Student ]

FREE 10+ Product Supply Proposal Samples in MS Word | Google Docs | Apple Pages | PDF

FREE 10+ Health Project Proposal Samples [ Public, Mental, Healthcare ]

FREE 11+ Engineering Project Proposal Samples in PDF | MS Word

FREE 4+ Racing Sponsorship Proposal Samples [ Team, Car, Driver ]

FREE 10+ Nursing Project Proposal Samples [ Community, Health, Clinical ]

FREE 11+ Student Council Proposal Samples in PDF | DOC

FREE 10+ Facilities Management Proposal Samples in MS Word | Google Docs | Apple Pages | PDF

FREE 8+ Joint Venture Proposal Samples [ Commercial, Real Estate, Construction ]

FREE 10+ Scholarship Proposal Samples [ Project, Grant, Sponsorship ]

FREE 10+ Computer Purchase Proposal Samples in MS Word | Google Docs | Apple Pages | PDF

FREE 10+ Network Project Proposal Samples [ Design, Security, Bank ]

FREE 14+ Accounting Proposal Samples in PDF | MS Word

FREE 10+ Church Event Proposal Samples in MS Word | Google Docs | Apple Pages | PDF

FREE 10+ History Proposal Samples [ Dissertation, Thesis, Paper ]