Every business must keep track of their revenues and expenses so that they’ll know how money is acquired and spent by the business. Revenue is the amount that the company earns from its operations. In other words, it is the company’s income or profit. Expenses are cash payments that come from a portion of an asset, which directly reduces revenue. In accounting, the list of expenses that are recorded in accounting journals is called expense transaction entries. Let’s go more into detail about expense transactions.

What Is an Expense Transaction?

Expense transactions are an integral part of the processes of a business. It plays two important parts in the business processes because it is an inevitable part of earning profit and constitutes part of the costs of doing business. Business owners must understand that expenses are different from costs because, as mentioned, it is just part of the cost. Expense transaction entries are taken from business receipts of expenses, expense logs, and expense reports. The entries include wages, rent payments, supplies, debt write-off, etc. Expenses become part of income statements at the end of an accounting period. All of the expenses in that period are totaled and then deducted from the revenue of the business, which is then used in the calculation of the businesses’ net profit that is shown in the income statement.

There are two types of expenses that are recorded as expense transaction entries, and they are prepaid expenses and accrued expenses.

Prepaid expenses – refers to payments that are made in advance or before the payment due date. It is convenient for most companies to make advance payments instead of making recurring payments. For example, a company may opt to pay their health insurance for the whole year upfront, instead of making monthly payments. An adjustment is made in the accounting journal at the end of each month, where the prepaid insurance asset is decreased, and the insurance expense is increased.

Accrued expenses – are expenses that are not yet paid but are already recorded on the books but are recorded on the accounting period when it is incurred. An example would be when a company makes a purchase from another company or vendor but has not yet received an invoice for the purchase. The cost of the purchase is recorded even if the balance is not yet paid.

How to Record an Expense Transaction

You may find accounting and related tasks intimidating, but if you know what to do and how to do it, then there’s no such thing as an undoable task. Recording expense transactions is similar to entering payroll journal entries in a way because they’re both logged in an accounting journal and calculated at the end of the accounting period where they fall under.

1. Gathering of Information

Entering journal entires is not that simple. Before you do so, you’ll need proof of the transactions that is why you need to gather information from expense receipts, payment receipts, invoices and other relevant documents. If you don’t have these proofs, you cannot enter that expense into your accounting journal.

2. Determine Payment Method

The next step is to determine the payment method used by your company. Did your company paid with cash or did they use credit? It’s still payment made, but it makes a big difference when entered in your accounting journal.

3. Record the Expense

Once you have all the necessary details ready, you can go ahead and enter the expense transaction entries in your accounting journal. Entries must be detailed as possible, so you should include relevant information such as the transaction date, the dollar amount, the account number, account title, etc. Avoid making mistakes as much as possible, especially if you are doing handwritten journal entries. This will make your record seem unreliable.

4. Check If You Book Is Balanced

If your credit and debit are not balanced, then you’ll need to look for errors in your entries.

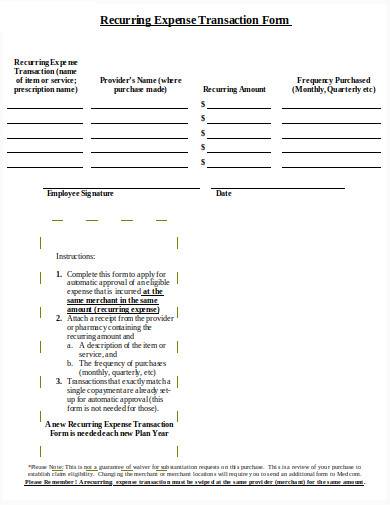

6+ Expense Transaction Samples in PDF | DOC

1. Expense Transaction Sample

2. Expense Transaction Template

3. Expense Transaction Example

4. Expense Transaction in PDF

5. Formal Expense Transaction Sample

6. Basic Expense Transaction Template

7. Expense Transaction in DOC

How are expenses treated in accounting?

Payment for expenses is taken from revenue. As revenue increases, expenses also increase. So when expenses incurred are increasing, you should use debit. The only time you credit expenses is when you need to make adjustments, reduce the expenses, or if you need to close the expense account. Expense accounts are Wage Expense, Rent Expense, Salaries Expense, Supplies Expense, etc.

How long do I need to wait before my work expenses are paid?

Some companies use the pay and reclaim method where the employees pay their work expenses from their own earnings. They reclaim this payment from their employers, which takes about four weeks. Many employees, especially those who don’t earn too much, do not reclaim these expenses because it’s either the amount is too little, or the process is frustrating and difficult to understand.

Do you consider reimbursements as expenses?

Expense reimbursement is a process where employers pay back their employees for the expenses they incurred that are work-related. For example, if you went on a business trip where you spend your own money for transportation, your company or employer is likely to reimburse or pay you back with how much you have spent for transportation during the trip. Just makes sure that you keep receipts as proof of the transaction. The accounting department will need it to enter the expense to the journal.

Learning about expense transactions and other accounting concepts can be frustrating, so you’ll need all the help that you can get from different sources. Luckily, we have free downloadable samples that you will surely love. You should definitely check them out!

Related Posts

9+ Sample Check Request Forms

FREE 14+ Travel Expense Statement Samples

9+ Sample Checkbook Registers

14+ Sample Profit and Loss Statements

11+ Business Receipt Templates

8+ Sample Credit Card Payment Calculators

10+ Sample Lists of Expenses

FREE 10+ Weekly Budgets

49+ Claim Forms Examples

Sample Schedule C Forms

7+ Travel Quotation Templates

8+ Sample Petty Cash Log Templates

What Is a Receipt Format

5+ Sample Business Valuation Reports

29 Printable Accounting Forms