Securing adequate money to fund a company’s operations is a crucial aspect of running a corporation. Borrowing money is a popular method of accomplishing this. This is also known as debt financing because it comes with the promise of repaying the lender at a later date. It’s critical to retain documentation that clearly specifies each party’s legal rights and obligations, whether you’re the borrower or the lender. A simple promissory note, loan agreement, debenture agreement and register of debentures, or deed of charge, to name a few examples, could be used in this situation.

10+ Deed of Charge Samples

A deed of charge is a legal document that marks an agreement between two businesses in which one business lends money to the other and acquires a security interest in the borrower’s assets. This creates a charge against the borrower’s property, requiring the borrower to surrender their assets to the lender if the debt is not repaid. As a result, it’s effectively a mortgage for company debts secured by business property (such as manufacturing machinery). Indeed, having a mortgage to acquire a home loan from a bank, for example, is similar.

1. Deed of Charge

2. Sample Deed of Charge

3. Bank Deed of Charge

4. Company Deed of Charge

5. Legal Deed of Charge

6. Simple Deed of Charge

7. State Deed of Charge

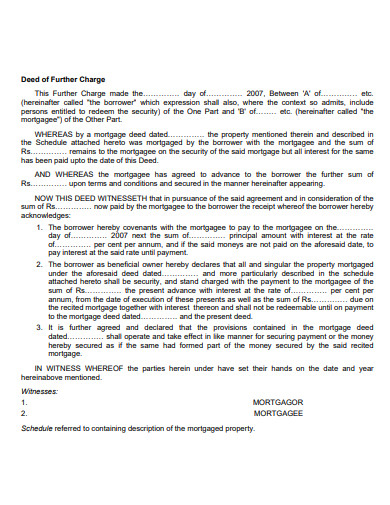

8. Deed of Further Charge

9. Professional Deed of Charge

10. Registration Deed of Charge

11. Printable Deed of Charge

Prior to 2012, deeds of charge required to be registered with ASIC within 45 days to be effective. Personal property charge deeds must now be recorded on the Personal Property Securities Register (PPSR) within 20 business days of being created. Failure to do so may jeopardize the lender’s entitlement to the property if the borrower fails to repay them. Furthermore, failing to register the deed in a timely manner may result in competing claims to the property. These claims could ultimately take precedence over the lender’s interests. Most importantly, personal property refers to any sort of property that is not land in this context.

How Does it Helps?

The main advantage of a deed of charge for borrowers is that it expands their available resources. Borrowers may now not only sustain their cash flow, but also expand their businesses.

A deed of charge protects lenders from losing money if the borrower defaults on their payments. This is due to the fact that it gives them authority over the borrower’s assets in the event of default. It also reduces the danger of the borrower defaulting on the loan in the first place, thanks to the lender’s ability to seize the borrower’s assets if they default.

A deed of charge can also require compromise by establishing an enforceable agreement with strongly outlined rights and responsibilities. Indeed, it aligns both firms’ expectations about how payments to the lender should be paid and what the penalties will be if these requirements aren’t met. It can also include information such as what insurance and continuing business practice duties each party has.

A Deed of Charge is a contract between two corporations that establishes a charge (security) against the borrower’s assets (plant, machinery, goodwill, and so on) in exchange for loan repayments. The charge is usually in the form of a “fixed and floating” charge, meaning it attaches to both tangible and intangible assets, such as plant and machinery (fixed) and goodwill and fluctuating bank account balances (floating) (floating). Charge deeds are essentially mortgages on commercial assets used to secure company debts. For a Deed of Charge to be effective, it must be registered with ASIC within 45 days of its establishment.

FAQs

Why do you need a deed of charge?

- Deeds of Charge safeguard your capital investment in a business.

- In the event of default, Deeds of Charge give you control over corporate assets.

- Charge deeds are legally binding.

- Not all Deeds of Charge are suitable for all types of enterprises. GJA Law can provide you with specific guidance and tailor-made solutions based on your unique circumstances.

- Consequences of Not Having Charge Deeds

- Customers may delay payments far beyond your expectations, and you may not be able to charge interest on the money you don’t receive.

- If payment is not made, you may not be able to retrieve business assets because ownership has been transferred.

- You can’t control what happens in the event of a disagreement.

- Deeds of Charge provide security.

When can you use a deed of charge?

This Deed of Charge should only be used when a company is securing a debt or loan, and the party receiving the charge (the Mortgagee) is itself a corporation. The Mortgagee to whom the charge is being provided has lent money to the Company issuing the charge and may lend more money to the Company in the future, according to this Deed of Charge.

If you want to see more samples and formats, check out some deed of charge samples and templates provided in the article for your reference.

Related Posts

Sample Business Card Templates

Sample Cashier Job Descriptions

Questionnaire Samples

FREE 10+ Sample HR Resource Templates in PDF

FREE 10+ HR Consulting Business Plan Samples in MS Word | Google Docs | Pages | PDF

FREE 49+ Sample Job Descriptions in PDF | MS Word

FREE 16+ Nonprofit Budget Samples in PDF | MS Word | Excel | Google Docs | Google Sheets | Numbers | Pages

FREE 13+ Academic Calendar Templates in Google Docs | MS Word | Pages | PDF

FREE 10+ How to Create an Executive Summary Samples in Google Docs | MS Word | Pages | PDF

FREE 23+ Sample Event Calendar Templates in PDF | MS Word | Google Docs | Apple Pages

Company Profile Samples

FREE 10+ Leadership Report Samples [ Development, Training, Camp ]

FREE 24+ Sample Payment Schedules in PDF | MS Word

FREE 10+ Return to Work Action Plan Samples in PDF | DOC

Autobiography Samples & Templates