Sometimes, business owners come to the decision of wanting to sell their business. If you have also come to this decision, you have to follow a checklist to ensure that you have everything covered, even the smallest details. Once you and a buyer have finalized everything about the sale, it is high time that you schedule the closing of the deal accordingly. We would like to give you a few tips on what you need to do when it comes to selling your business. We will let you in on the content of sample checklist templates regarding selling the business. Check it out right here.

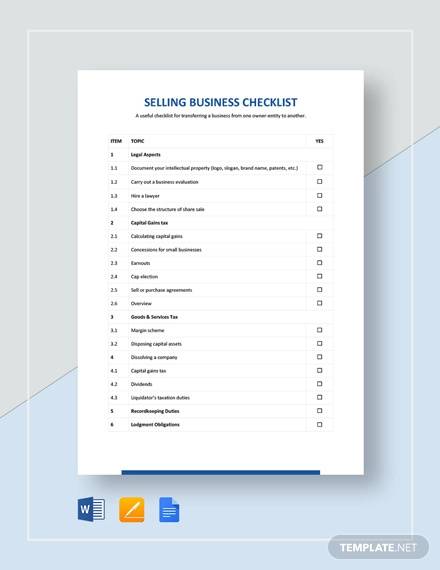

Selling Business Checklist Template

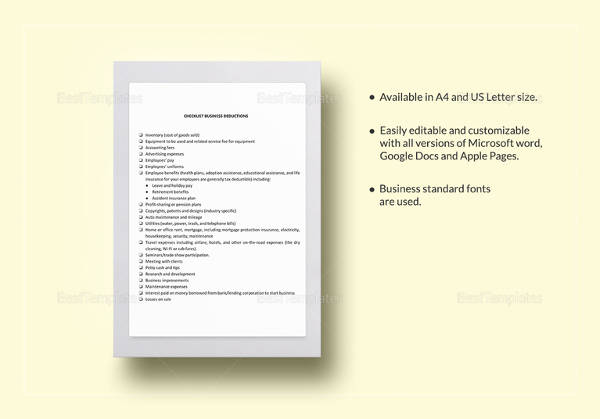

Business Deductions Checklist

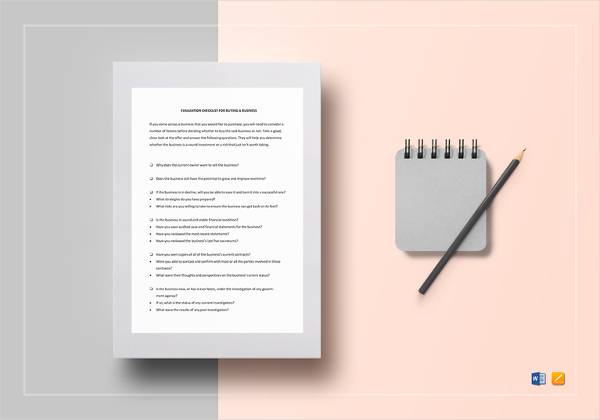

Checklist Sale of a Business Template

Prepare Yourself for Closing Day

Before closing your business, there are a few tasks that you need to take care of. Talk with your broker (if you have one), your accountant, and your lawyer to ensure that all the tasks you will be doing are necessary for your situation. Here is a sample task checklist template that would be helpful during the pre-closing days of your business.

- Schedule the day of closing your business. Choose a convenient day such as the last quarter of the year in order to simplify any proration of finances such as monthly expenses during the transfer of rights. The time of the day also matters. It should preferably be daytime in order for you to easily get in touch with banks and government offices.

- Finalize your price. Consider the prorated utility fees, rent/lease, receivables and payables, as well as the inventory value.

- Have corporate documents prepared. You can consult with your lawyer regarding the documents especially if your business is registered as a corporation as you need to consult with the rest of the shareholders as well.

- Prepare the tax forms and other government documents. This will include any transfer request forms for the business property, IRS forms, business transfer agreements, etc.

- Review and confirm the requirements of the business’s insurance. The details should be reflected in the purchase and sale agreement that you have with the buyer.

- Have the equipment list ready. You should also note in the list which ones are still under a lease. Prepare a list of assets that are not part of the sale as well.

- Prepare to transfer any contracts and agreements that you have. You have to take all of the necessary steps to ensure that all transactions when the sale has been done go on as smooth as possible.

- Finalize your list of receivables and payables. You may also include aging reports.

- Prepare building lease transfer. Prepare copies of the lease, lease amendments, and lease agreements.

- Prepare the bill of sale. The real estate bill of sale will be the official document that will serve as the record that the sale between you and the buyer has occurred.

- Have a settlement sheet prepared. This will have all the prices such as purchase price, price adjustments, and other costs. Your lawyer will be the one to help you prepare the settlement sheet.

Scheduling the Closing

There are two ways of closing the sale of your business. It can be done through an escrow account or through your attorney’s office.

If you close the sale in an escrow office:

- Follow the instructions provided in the escrow account.

- Obligations and contingencies will be provided by the escrow officer. It will be listed in the letter of intent to purchase.

- You and your buyer will now have to sign the closing documents.

- The transfer of funds and the record of the sale will be done by the escrow agreement agent.

If you close the sale in your lawyer’s office:

- Your lawyer, as well as the lawyer of the buyer, will prepare the deed of sale and the purchase agreement.

- Address any outstanding obligations or contingencies. This will be reflected in the sample agreement.

- Everyone involved with the sale—you, the buyer, and the lawyers—will meet to sign the documents and officially transfer the funds.

Review the Purchase and Sale Agreement

A purchase and sale business agreement form will be provided to you by either your broker or your lawyer. You can review it alongside the buyer to see if you would want to have any revisions to your agreement. Have your lawyer make the final review and have the proper descriptions of the obligations.

Finalize the Sale

- Ensure that everyone involved with the sale should be present. This involves lawyers (your lawyer and your buyer’s lawyer), shareholders, you, and the buyer.

- Agree to any adjustments post-closing such as prices, prorated expenses, closing valuation, inventory, and accounts receivable. Finalize all of these at least 15 days before the date of closing.

- Review and sign the agreement.

- Review and sign the documents for the loan.

- Review and sign transfer forms and documents for funds, patents, copyrights, etc.

- Review and sign the legal bill of sale.

- Review and agree on what is reflected on the settlement sheet.

- Review and agree to the transfer of documents regarding taxes.

- Receive the payment and issue a payment receipt.

After all that you went through, you are now done with the deal! However, there are more things that need your involvement to formally transfer your business to its new owner.

By following the checklist that we have provided, you will be able to easily ease the transfer of ownership to the new owner. Letting go of your business might not have been the easiest decision you have made but you know that it was for the best whatever reasons you might have for doing so. If selling your business for retirement reasons is still far off, that is okay. At least you are now prepared with a free checklist when the time to do so starts to come.

Before we end, we would like to leave you with a few DOs that will be helpful with the sale of your business:

- Keep all your records up to date.

- Make sure that you are always open for communication.

- Provide all the necessary information in advance.

- Keep your business in tip-top shape. Negligence of your day-to-day operations should never be an option.

We hope you find this article helpful and we wish you all the best!

Related Posts

FREE 18+ Complaint Checklist Samples in MS Word | Google Sheets | PDF

FREE 18+ Internship Checklist Samples in MS Word | Google Docs | PDF

FREE 18+ Statement Checklist Samples in MS Word | Google Sheets | PDF

FREE 20+ Voluntary Checklist Samples in MS Word | Google Sheets | PDF

FREE 18+ Summary Checklist Samples in MS Word | Google Sheets | PDF

FREE 14+ Sponsorship Checklist Samples in MS Word | MS Excel | PDF

FREE 18+ Conference Checklist Samples in MS Word | Google Sheets | PDF

FREE 17+ Lesson Checklist Samples in MS Word | Google Sheets | PDF

FREE 18+ Progress Checklist Samples in MS Word | Google Docs | PDF

FREE 18+ Enrollment Checklist Samples in MS Word | Google Docs | PDF

FREE 18+ Graduation Checklist Samples in MS Word | Google Sheets | PDF

FREE 15+ Consent Checklist Samples in MS Word | Google Sheets | PDF

FREE 18+ Review Checklist Samples in MS Word | Apple Pages | PDF

FREE 18+ Submission Checklist Samples in MS Word | Google Docs | PDF

FREE 18+ Request Checklist Samples in MS Word | MS Excel | PDF