According to the analysis of Marshall & Swift/Boeckh, there are more than 40% of businesses in the US have insurance policies. Surely, companies and businesses that fall in the percentage above are those who know that they must protect their companies with the backup and aid of insurance providers. But, what if during a personal injury trial, the plaintiff or the one who sued the company wins? That’s when a liability claim comes in, and that’s also when the insurance provider will pay for the plaintiff’s damages on behalf of the defendant or the policyholder. However, before giving the payment and any financial aid, insurance providers also conduct evaluations and claim assessments, too, to ensure that the policyholder’s insurance coverage indeed covers the claim. And guess what they use, aside from the obvious legal forms and affidavits that the plaintiff submitted? Well, a liability claim checklist, of course! Don’t know what’s in it? Then, read on to discover the significance and contents of this essential document.

FREE 5+ Liability Claim Checklist Samples and Templates in PDF

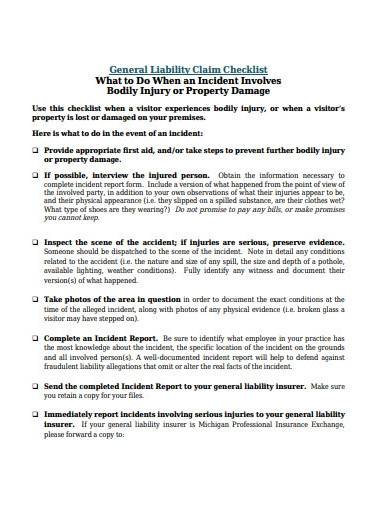

1. General Liability Claim Checklist

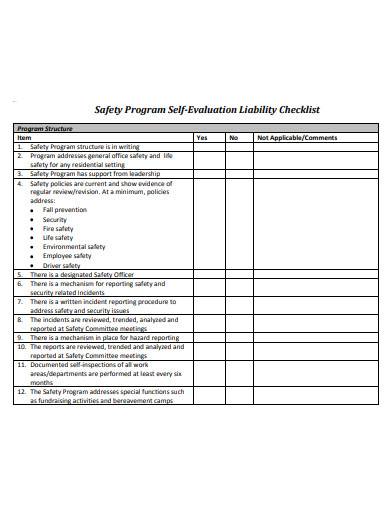

2. Program Self-Evaluation Liability Checklist

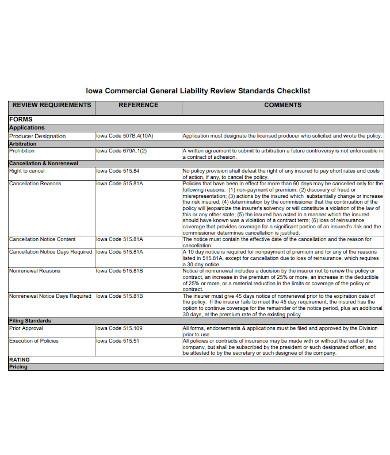

3. General Liability Review Checklist

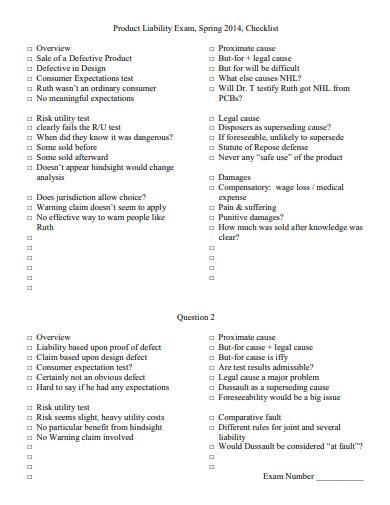

4. Product Liability Exam Checklist

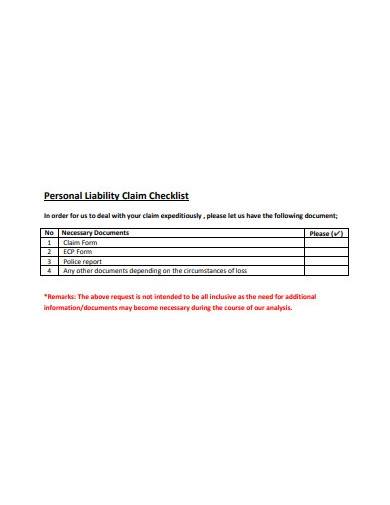

5. Personal Liability Claim Checklist

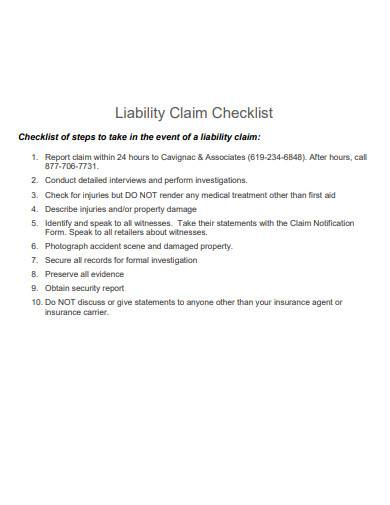

6. Liability Claim Checklist Template

How to Make a Liability Claim Checklist for Your Clients

Being an insurance agent can be a tough job, especially when it comes to determining what to do when dealing with those who are facing a business liability in a personal injury claim. So, if you’re one who has business owners mostly as your client, then you should keep the following tips in mind before you make your liability claim checklist:

1. Identify, List, and Categorize

Checklists, when done right, are useful for becoming productive. So, the first step that you must make is to identify what you want to put into your checklist. You can start by thinking of common and possible situations that your clients or policyholders can get into. For instance, if you have a client who manufactures and sells kitchen equipment, then you can focus on product liability claims. Then, you can proceed to list the liability evaluations that you are going to take if ever your client’s customer ends up suing him or his company due to faulty equipment that caused personal injuries. After that, you can head on to categorizing the evaluation items based on their relevance and connections.

2. Remove Anything Unnecessary

Have you ever tried making a grocery list, and ended up crisscrossing some items you listed before you even arrived at the store? Well, that’s because you realized that you didn’t need those items, right? So, you must do the same when making your checklist and any document that you will be making in the future. Just go through each item that you are including in your liability claim checklist and determine whether or not it’s necessary. This not only helps you make an efficient list but also aids you in making a simplified document.

3. Don’t Forget the Legal Areas

They say that in life, it’s not all black and white. And when we apply that to your aim in determining the validity and eligibility of a liability claim, it means that it’s not all about your preferences, needs, and the requirements of the insurance company that you’re working in, but also the legislation and laws of the state. You must be knowledgeable in the legal area of providing and catering to personal injury payments, fees, and other technical aspects of liability claims.

FAQ’s

Is a liability claim checklist a legal form?

No, a liability claim checklist is not a legal form. It is only intended to be used as a tool for verification and preparation purposes. But, when used in the period of a case trial in court, specifically those related to its use or to a company’s business and product liability lawsuit, then you can keep the checklist along with other legal forms for record-keeping.

As an insurance provider, why should I use a liability claim checklist?

A liability claim checklist will help you be more organized and goal-oriented. Also, it will aid you in verifying and determining liability claims eligibility, and how much of the insured’s policy can cover a liability case faced by the insured who’s also your client.

I am not an insurance provider or agent, but I am an insured business owner. Can I use a liability claim checklist?

Yes, you can use a liability claim checklist. However, it should be mainly for identifying situations in which you will be liable for or for your personal use as a means of determining your business’s liabilities, responsibilities, risks, and potential problems.

Are the above-listed liability claim checklist samples and templates free to use and editable?

Yes, all our sample forms and templates, including those listed above, are free and editable. Just choose, then hit the blue download button that’s situated at the right side of the template’s image, then extract the template from the downloaded zip file, and off you go to editing its contents.

Can I reuse the liability claim checklist samples and templates that I downloaded from your site?

Absolutely! You can reuse, edit it again, and fill it out in the future if you want to. You can even update its layout and add your own customized designs and elements to incorporate your insurance company’s branding preferences. And the best part is, our templates are available in a file format that’s compatible with all sorts of devices so that you can have it anytime and anywhere you need it!

Liability claim checklists may not be one that’ll have the notarization of an attorney, nor is it a document that a judge uses in a liability and personal injury case, but it’s an essential tool for insurance companies like yours. So, go ahead and choose which among our templates suits your needs now, before any of your policyholders requires your insurance expertise for dealing with a case that their customers filed against them!

Related Posts

FREE 3+ Job Handover Checklist Samples in PDF

Toilet Cleaning Checklist Samples & Templates[ Room, Deep Inspection ]

Handover Checklist Templates

FREE 10+ Equipment Inspection Checklist Samples [ Safety, Daily, Maintenance ]

FREE 10+ Turnover Checklist Samples [ Project, Apartment, Cleaning ]

FREE 12+ Vehicle Maintenance Checklist Samples [ Preventive, Service, Routine ]

FREE 20+ House Checklist Samples in MS Word | Google Docs | Apple Pages | PDF

FREE 18+ Hospital Bag Checklist Samples in MS Word | Google Docs | PDF

FREE 20+ Student Enrollment Checklist Samples in MS Word | Google Docs | PDF

FREE 18+ Improvement Checklist Samples in MS Word | Google Docs | Apple Pages | PDF

FREE 23+ Education Checklist Samples in MS Word | Google Docs | PDF

FREE 21+ Course Checklist Samples in MS Word | Google Docs | PDF

FREE 11+ Freelancer Checklist Samples in MS Word | Google Docs | PDF

FREE 23+ Party Checklist Samples in MS Word | Google Docs | Apple Pages | PDF

FREE 18+ Scheduling Checklist Samples in MS Word | Google Sheets | PDF