8+ Small Business Profit and Loss Samples

As a small company owner, you must have a thorough awareness of both your revenue and costs. That is why keeping track of both is critical. It keeps you organized, prepares you for tax season, and builds on your success by providing a clear and scientific approach to managing your funds. It helps you keep on top of your business in general. Checking your profit and loss statement is one approach to keep track of it. Need some help writing this? We’ve got you covered! In this article, we provide you with free and ready-made samples of Small Business Profit and Loss in PDF and DOC format that you could use for your benefit. Keep on reading to find out more!

1. Strategies Minimize Profit Loss Small Business

2. Small Business Profit and Loss Statement

3. Profit and Loss Small Business Administration

4. Profit and Loss Financing Small Business

5. Small Business Finances Profit and Loss

6. Employment Small Business Profit and Loss

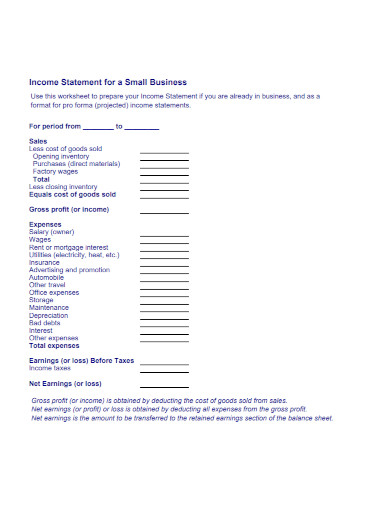

7. Income Statement Small Business Profit and Loss

8. Small Business Statement Profit and Loss

9. Financial Literacy of Small Businesses Profit and Loss

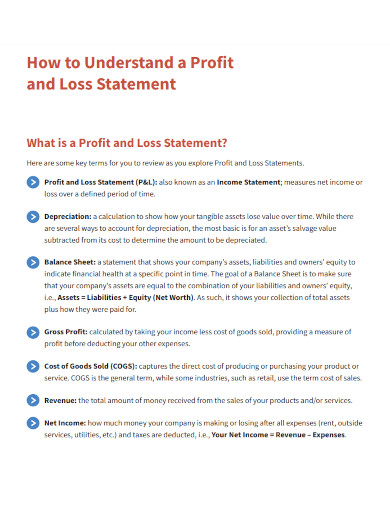

What is a small business profit and loss?

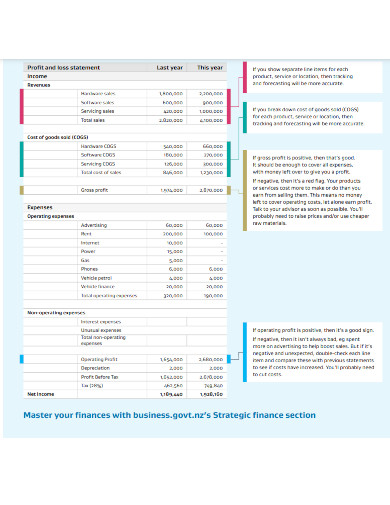

The heart of a small business accounting is a profit and loss statement. A profit and loss statement summarizes a company’s income and spending over a certain time period. This is also known as an income statement, profit statement, statement of operations, or profit and loss report. Whatever word is chosen to describe this financial statement, it represents a snapshot of a company’s income and spending during a given time period. This is often done at least quarterly and yearly, although it can be done more regularly. Profit and loss statements are often generated on a monthly, quarterly, or yearly basis.

A small business profit and loss

Analyzing revenues and costs by line item and comparing amounts to earlier quarters aids in identifying positive and negative company trends. A Small Business Profit and Loss Template can help provide you with the framework you need to ensure that you have a well-prepared and robust statement on hand. To do so, you can choose one of our excellent templates listed above. If you want to write it yourself, follow these steps below to guide you:

1. Begin with the income.

For small enterprises, revenue is stated first on a profit and loss statement and includes all income components. This might be sales, gross revenues, fees, or any other phrase used to characterize the company’s operational revenue. Revenue is recorded as generated, at the moment of sale, when adopting the accrual method of accounting, even if payments have not yet been received. When using the cash method, revenues are recorded when payment is received.

2. List your costs.

For small firms, the expense section of a profit and loss statement includes any cost made to run the business. Understanding asset depreciation is required when accounting for various costs. Some acquisitions, such as office equipment, must be capitalized as an asset and depreciated throughout the item’s useful life. Every year, 20% of the cost of the equipment is shown in the profit and loss statement.

3. Input your gross profit.

The difference between revenue or gross revenues and the cost of items sold is the gross profit. If the firm is a service business with no inventory, the gross profit and gross revenues are equal.

4. Calculate the net profit and loss.

Upon deducting any taxes owed from pretax income, the net amount equals a company’s profit or loss for the period. When comparing organizations in various industries and tax conditions, or when exact figures aren’t yet available, net profit or loss is sometimes equated to profits before interest, taxes, depreciation, and amortization.

FAQ

What exactly is a profit and loss example?

For a shopkeeper, for example, if the selling price is greater than the cost price of a commodity, it is a profit; if the cost price is greater than the selling price, it is a loss.

How much profit should I make from my business?

If you have an accountant or tax preparer, ask them what proportion of your net income you should set aside for taxes. Because they will be aware of your specific tax status, they will be able to provide you with a more precise percentage.

How many companies turn a profit in their first year?

Most firms do not generate a profit in their first year. In reality, most new enterprises require 18 to 24 months to become profitable.

These statements are crucial since many businesses are compelled to complete them by legislation or association membership. To help you get started, download our easily customizable and comprehensive samples of Small Business Profit and Loss today!

Related Posts

Weekly Schedule Samples & Templates

Contractual Agreement Samples & Templates

FREE 9+ Amazing Sample Church Bulletin Templates in PSD | PDF

Sample Business Card Templates

Sample Cashier Job Descriptions

Questionnaire Samples

FREE 10+ Sample HR Resource Templates in PDF

FREE 10+ HR Consulting Business Plan Samples in MS Word | Google Docs | Pages | PDF

FREE 49+ Sample Job Descriptions in PDF | MS Word

FREE 16+ Nonprofit Budget Samples in PDF | MS Word | Excel | Google Docs | Google Sheets | Numbers | Pages

FREE 13+ Academic Calendar Templates in Google Docs | MS Word | Pages | PDF

FREE 10+ How to Create an Executive Summary Samples in Google Docs | MS Word | Pages | PDF

FREE 23+ Sample Event Calendar Templates in PDF | MS Word | Google Docs | Apple Pages

Company Profile Samples

FREE 10+ Leadership Report Samples [ Development, Training, Camp ]