What comes to mind when you hear the word journal? Well, there are basically two types of journals. If you’re a writer, a journal would be some form of diary. For accountants, journals are books used in recoding financial transactions. In this article we will be discussing about the latter. As you can see, the samples below show a wide range of downloadable journal entry templates. We’ve also provided steps on how you can make a simple journal entry.

FREE 10+ Journal Entry Templates in PDF

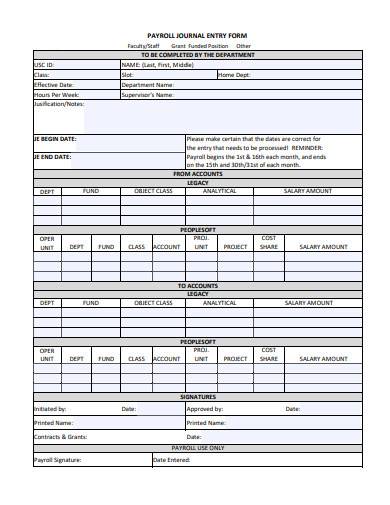

1. Payroll Journal Entry Form Sample

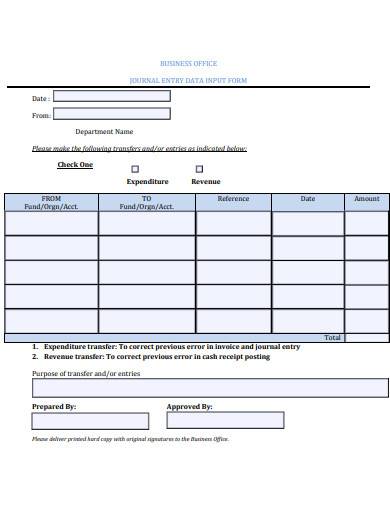

2. Journal Entry Data Input Form Template

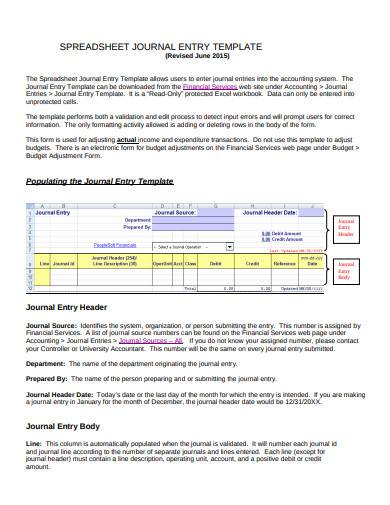

3. Journal Entry Spreadsheet Template

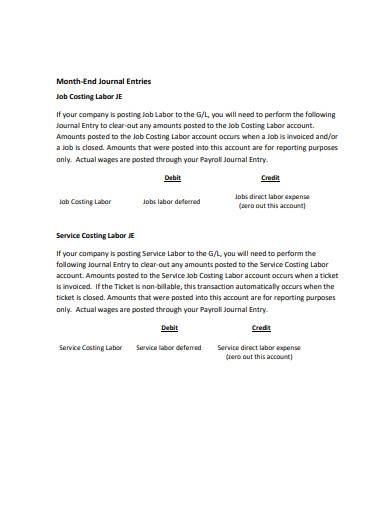

4. Month End Journal Entry in PDF

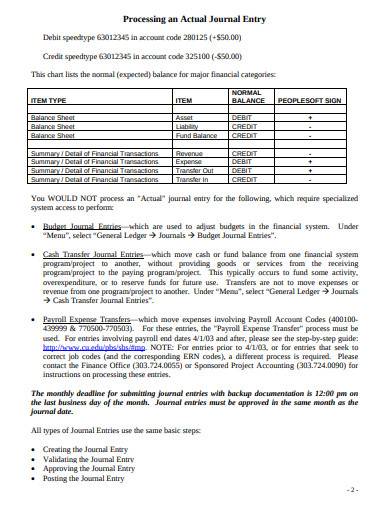

5. Journal Entry System Form

6. Online Journal Entry Template

7. Journal Entry Template

8. Printable Journal Entry Template

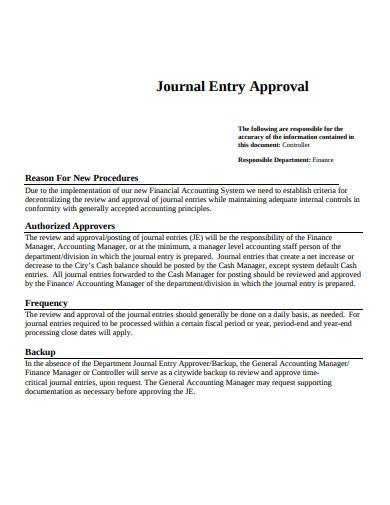

9. Journal Entry Approval Template

10. Journal Entry Process Template

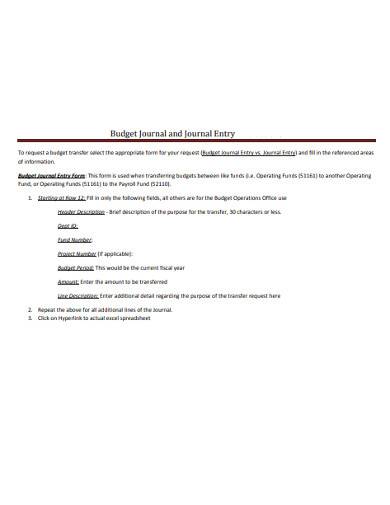

11. Simple Budget Journal Entry Template

What Is a Journal Entry?

Companies keep accounting books to record and track all their business-related transactions. The process of recording business-related financial information is referred to as a journal entry. The financial information includes accounts, expenses, payroll, inventory, accrued interest, amortization, bad debt expenses, etc. Journal entries provide an audit trail for specific accounts and is also known as the first step taken in the accounting cycle. This allows organizations to analyze the consequences of their actions and determine their effects on the companies financial status.

A journal entry reflects the movement of cash of the business. It is generally made of multiple credits and debits, where the sum of all credits must be equal to the sum of all debits. If this is not the case with your calculations, then it means that your journal entry is not balanced. You may need to go over your entries and computations to determine where you made a mistake. It is just like a balance sheet where the total assets must be equal to the total liabilities + shareholder’s equity of a company.

How To Make a Journal Entry

For some, working on an accounting ledger is an intimidating task. Well, if you think of all those figures you’ll be dealing with in that ledger, you would feel the same. But not all journal entries are complicated. There are instances when the entries are simple and manageable. If you want to become familiar with its format, then checking out journal entry examples for students will be a great help. To provide you with additional assistance, here are basic steps that will help you get your accounting journal entry started.

1. Follow a Basic Journal Entry Format

There are ready-made journal entry templates online that are available for download. Use these sample templates as your reference to help you build the layout of your accounting journal. If you’re lucky, you may even find a customizable template. Choosing a simple template is important if you don’t want to get lost or get confused with what you’re doing. However, this is only applicable to simple transactions.

2. Write Down the Required Information

Fill in the blanks or spaces in the template with the required information, such as the account name, the debit amount, the credit amount, etc. If you’re having problems completing the accounting form, then you can get help from journal entry examples. If this doesn’t help, then you can always ask journal entry questions from experts or get answers online.

3. Make Adjustments to the Entries

After supplying all the required information, the next step would be to debit and credit each account. So, how is it done? Aside from wrong journal entries, debits and credits make up most of the mistakes in an accounting book. The three golden rules of accounting will help you avoid mistakes, and they are as follows:

- Debit what comes in, credit what goes out

- Debit the receiver, credit the giver

- Debit all expenses and losses, credit all incomes and gains

4. Balance the Debit and Credit

When you’re done making the necessary adjustments, you’ll need to check if your work is accurate. To do this, you’ll need to calculate the ending balance of each account. Both sides must stay balanced. If they are not, then you’ll need to go over your work and find the mistake. Once it’s all good, update your company’s balance sheet template.

FAQs

What is the purpose of a journal entry?

When you think of how businesses value journal entries for their company, you know that they have a purpose. The purpose of a journal entry is as follows:

- It is considered as the foundation of all financial reports.

- It records financial business transactions as they occur.

- It shows the specific accounts that are affected by the transactions.

- Auditors use the information provided by journal entries to analyze the impact or effect of the financial transaction to a business account.

- The balances in a journal entry are calculated, and the results are used to update the balance sheet.

What should I include in a journal entry?

Your journal entry should have the following information:

- Title/header

- Date of the entry

- Journal entry number or a reference number

- Account name

- Account number

- Debit amount (in the second column)

- Credit amount (in the third column)

- Description of the journal entry (footer)

What is double-entry bookkeeping in journals?

Double-entry bookkeeping means that two account entries must be recorded in every business transaction. One entry is a debit, and the other a credit. An example is when recording a sales revenue amounting to $700. On your credit entry, you should put $700 to increase the revenue of your income statement. The debit entry is also $700 to increase the cash account on your balance sheet.

Practice makes perfect. If you’re not good with journal entries, you can always improve through constant practice. And a great way to practice is by using the journal entry templates that we’ve provided above. Don’t get stuck. Get motivated!

Related Posts

Ukulele Chord Chart Samples & Templates

Retirement Speech Samples & Templates

Weekly Schedule Samples & Templates

Contractual Agreement Samples & Templates

FREE 9+ Amazing Sample Church Bulletin Templates in PSD | PDF

Sample Business Card Templates

Sample Cashier Job Descriptions

Questionnaire Samples

FREE 10+ Sample HR Resource Templates in PDF

FREE 10+ HR Consulting Business Plan Samples in MS Word | Google Docs | Pages | PDF

FREE 49+ Sample Job Descriptions in PDF | MS Word

FREE 16+ Nonprofit Budget Samples in PDF | MS Word | Excel | Google Docs | Google Sheets | Numbers | Pages

FREE 13+ Academic Calendar Templates in Google Docs | MS Word | Pages | PDF

FREE 10+ How to Create an Executive Summary Samples in Google Docs | MS Word | Pages | PDF

FREE 23+ Sample Event Calendar Templates in PDF | MS Word | Google Docs | Apple Pages