Carrying multiple debts at once can be overwhelming, and determining where to focus your repayment efforts first can be difficult. Plus, the longer you keep your debts open, the more interest you pay over time, exacerbating the problem. Finding a debt repayment strategy that works for you and your specific financial situation is critical. That way, you’ll know exactly where to direct your payments to have the greatest impact on your debt. There are two main methods you can use to decide which debts to pay off first: the highest-interest-first plan and the snowball plan.

10+ Debt Repayment Agreement Samples

It’s important to prioritize your debt payments in relation to one another, but you also have to think about them in the context of your other expenses. Remember that before you concentrate on getting out of debt, you must first make sure that your basic living expenses are covered and that you are not going over your monthly budget while working on repayment.

1. Debt Repayment Agreement Template

2. Authorization Debt Repayment Agreement

3. Debt Repayment Agreement Form

4. Temporary Debt Repayment Agreement

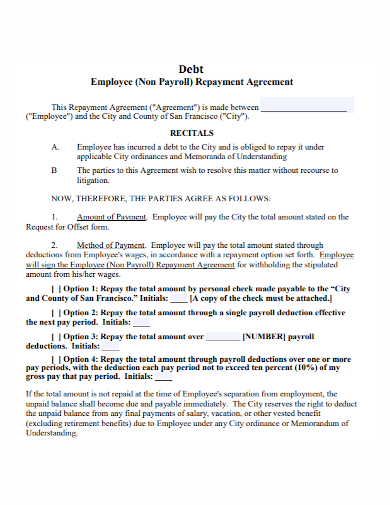

5. Employee Debt Repayment Agreement

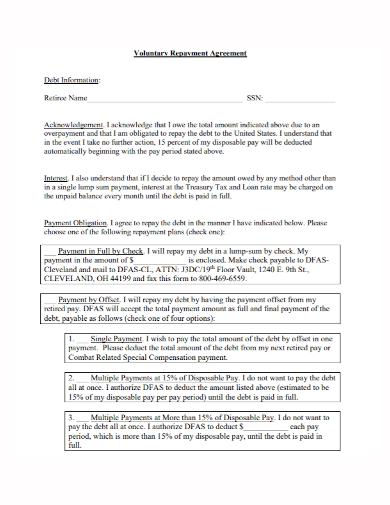

6. Voluntary Debt Repayment Agreement

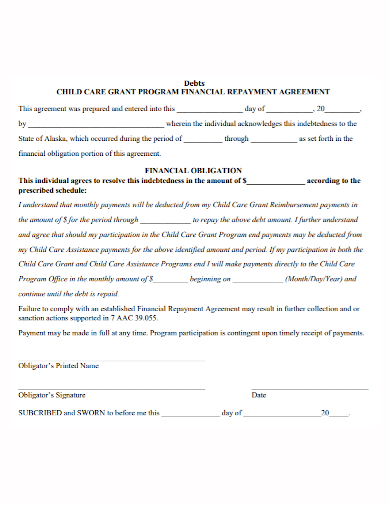

7. Financial Debt Repayment Agreement

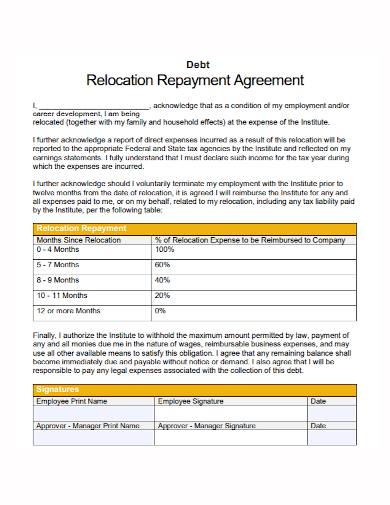

8. Debt Relocation Repayment Agreement

9. Debt Repayment Assurance Agreement

10. Debt Repayment Policy Agreement

11. Bank Debt Repayment Agreement

Highest-Interest-First Plan

Even if the value of principal you owe (your balance before having to add any interest) is the same, debts with a higher interest rate will cost you more money in the long run than debts with a lower interest rate. For example, if you have a $10,000 auto loan with a 4% interest rate and five years to pay it off, you’ll end up paying $11,049.91 in total. The same loan paid over the same period but with a 6% interest rate, will cost you $11,599.68, a difference of more than $500. Paying off the debts with the highest interest rates first can help you save money in the long run.

If you choose the highest-interest-rate strategy, make a list of your debts in order of highest to the lowest interest rate. Continue to pay the bare minimum on all of them, but put any extra cash you have toward the debt with the highest interest rate. After you’ve paid off that debt, move on to the one with the next highest interest rate, and so on, until you’ve paid off all of your debts.

Debt Snowball Plan

The snowball plan is a debt repayment alternative. This strategy requires you to always make all minimum monthly payments, but instead of organizing debts by interest rates, you focus your extra cash on paying off the smallest balance first. Once that one is paid off, apply the money you were paying each month to the next-smallest balance, along with the minimum payments you were already making on that account.

Once the second debt is paid off, you put all of the money you were paying each month toward the next-smallest debt, and so on, building momentum like a snowball rolling downhill.

FAQs

What is the difference between a debt avalanche and debt consolidation?

Debt avalanche: You pay off the highest-interest debt first (while paying minimums on the others), then the next-highest-interest debt, and so on. It could help you save time and money as you pay off your debts.

Consolidate multiple old debts into a single new one, preferably with a lower interest rate, to make payments more manageable or the payoff period shorter. Balance transfer cards and personal loans are two options for debt consolidation.

What is a debt management plan?

A nonprofit credit counseling agency can set up a debt management plan to lower your interest rate and put you on a repayment plan if you have a mountain of credit card debt and aren’t making much progress.

Is there a better way to pay off your debt than paying it off as is, or is there a faster way to pay it off? Check out the debt repayment agreement samples and templates provided in the article for your reference if you want to see more samples and formats.

Related Posts

FREE 10+ Mentoring Agreement Samples In MS Word | Apple Pages | PDF

FREE 10+ Partner Agreement Samples In MS Word | Google Docs | Apple Pages | PDF

FREE 10+ Individual Agreement Samples In MS Word | Google Docs | Apple Pages | PDF

FREE 10+ Strategic Agreement Samples In MS Word | Google Docs | Apple Pages | PDF

FREE 10+ Equity Agreement Samples In MS Word | Google Docs | Apple Pages | PDF

FREE 10+ Producer Agreement Samples in MS Word | Apple Pages | PDF

FREE 10+ Grant Agreement Samples In MS Word | Apple Pages | PDF

FREE 8+ Meeting Agreement Samples in MS Word | Google Docs | Apple Pages | PDF

FREE 10+ Community Agreement Samples In MS Word | Google Docs | PDF

FREE 8+ Real Estate Option Agreement Samples in MS Word | PDF

FREE 10+ Call Option Agreement Samples In MS Word | PDF

FREE 10+ Advertising Agreement Samples In MS Word | Google Docs | Apple Pages | PDF

FREE 10+ Car Agreement Samples In MS Word | Google Docs | Apple Pages | PDF

FREE 10+ Horse Agreement Samples In MS Word | Apple Pages | PDF

FREE 10+ Option Agreement Samples In MS Word | Google Docs | Apple Pages | PDF